Basic Fit N.V. (BFIT)

Basic Fit is Europe's largest gym chain. However, its share price is in need of more muscle.

Executive summary

We review Basic-Fit, Europe’s largest gym chain with presence in Western Europe.

With health benefits and gym membership below the US, Basic Fit has long-term tail winds to grow.

A new strategic acquisition of Clever Fit opens the DACH region and the option of licensing.

Constant reinvestment in its business hides Basic Fit’s free cash flow generation.

After the impact of the Covid pandemic, the markets have forgotten about this company.

Introduction

Basic Fit’s history starts back in 1984 when Rene Moos, former tennis player, created a tennis club and a sports gym. However, it is only in 2010 that what we know today as Basic Fit start taking shape. It was first acquired by Health City, Rene’s original business, when it had 28 gyms in the Netherlands. It quickly positioned itself as a low-cost gym operator following the model of Planet Fitness and subsequently sold Health City to remain as Basic Fit. After entering Spain and France, it listed in 2016 in the stock exchange, and by 2019 it had reached 2 million members. With a footprint in France and Benelux, it consolidated its position as a clear market leader in France. Fast-forward to 2025, and the strategic acquisition of Clever Fit, largely a licensing gym chain in the DACH region takes Basic Fit to new markets and to a new type of business it intends pursuing: licensing.

Business model

Operating markets

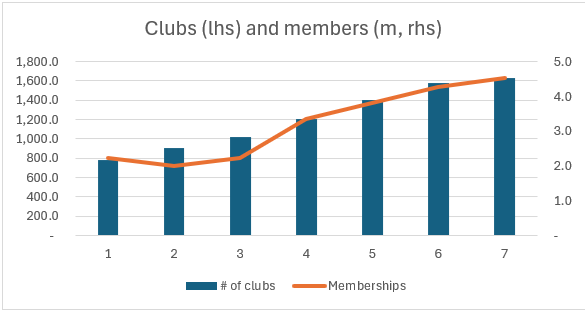

Basic Fit operates in the Benelux, France and Spain as core markets. It has further entered Germany, where it is taking market share at speed. Basic Fit operates under a strategy of clustering gyms, which means entering a city in one go with several gyms.

Source: Basic Fit investor presentation

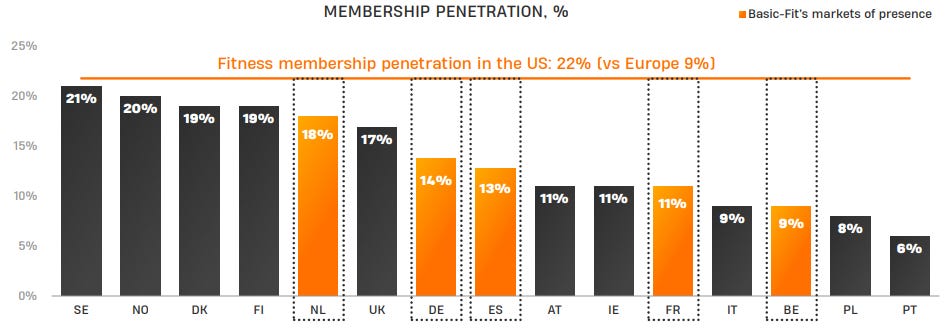

As shown on the above graph from Basic Fit’s investor presentation, the proposition to European customers is clear. There is severe under penetration of gym membership in Europe compared to the US. Underpinned by a cost of living crisis and risks to health such as obesity, Basic Fit’s low-cost gym proposition aims to benefit from those tailwinds.

Source: Basic Fit investor presentation

As for its presence, it has a strong presence in France and the Benelux but the potential and space to grow remains large, in particular in Spain and Germany. Overall, the company estimates being able to reach north of 3,000 gyms in these countries. Spain and Germany potential are in line with the low gym penetration levels in the population shown in the graph above.

Market positioning

Basic Fit is positioned as a low-cost gym chain. In order to work, this requires both scale and an attractive price-point. By clustering its gyms and offering the option to use any gym under their brand, members get better value for money than if they had access to a single gym. In addition, they push forward offers to bring for free on friend which increases engagement and customer retention, and the gyms are operated with minimal number of employees and has a large software component to it. Finally, Basic Fit is moving into a 24/7 gym offering, which is already showing positive results as it allows members to go to the gym at any time - thus accommodating to gym member schedules - all aimed at increasing client retention and average revenue per member.

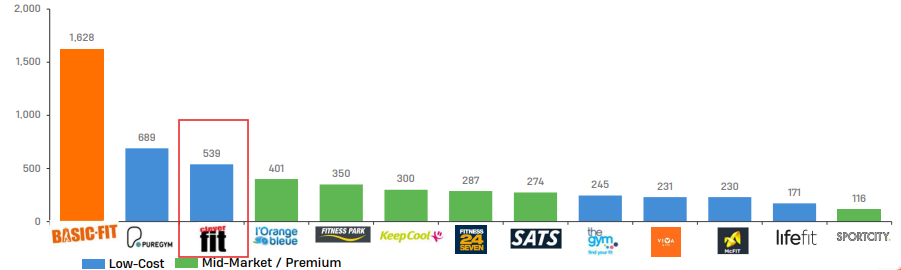

Competition is a reality and pricing power is somewhat limited. However, not many gyms have the geographical wrath of Basic Fit, as the below graph from the company indicates. In blue are the other low-cost gym chains in Europe. The second one, Clever Fit, has now been acquired by Basic Fit. The first one, Puregym, is focused in the UK, where Basic Fit does not operate anyway. Therefore, competition at European level is more limited. It is worth noting that Planet Fitness is entering the European market, but the level of fragmentation and market potential allows for multiple players.

Source: Basic Fit investor presentation

Business economics

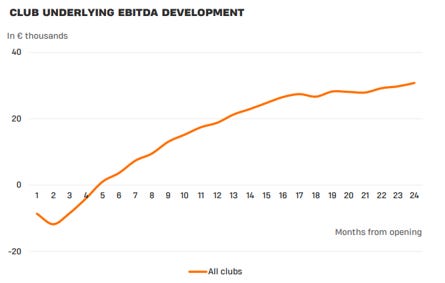

The economics of Basic Fit can be broken down by the profitability at gym level. When Basic Fit opens a gym, it is a immature club. It is only considered mature when the gym is, at the beginning of the calendar year, at least 24 months old. So, on average gyms reach 30 months before being mature. In order to break-even, a gym needs to reach, on average, 1,500 members. The gym’s costs are largely fixed: fixed number of employees, rent, equipment and software. Over time, the target number of members a mature gym aspires to get to is 3,250. In addition, the Board of Basic Fit will only approve opening a gym if the Return On Invested Capital (ROIC) is >30%. At the end of 2024, the ROIC on mature clubs stood at 34%. As a result, the payback period is between 3 and 4 years.

Example of a gym: Basic Fit spends about EUR 1.3m in a new gym. Over 3 years it will converge towards >3,000 members, a which point it will generate around EUR 1m in revenue. Deducting from that operating expenses (gym staff and rent) leads to a Club EBITDA less rent of EUR 460k / year, which divided by the initial investment equates to a ROIC of 37%.

Source: Basic Fit investor presentation

Now that the business model is reviewed, I have highlighted Club EBITDA as a business metric to follow. That is the EBITDA generated from running the gyms. For an even better metric, Club EBITDA less rent. Basic Fit runs a Club EBITDA margin of 60% and a EBITDA (Club EBITDA less overheads, so SG&A) of 48%. Then comes Depreciation at 16.5% of sales, amortisation of intangibles at 1% of sales (mostly their software) and rent (known as right-of-use depreciation) at 19% of sales. This leaves an operating profit at around 10% (10% to 12%). Those are the economics of Basic Fit.

Therefore, the business model is simple. The more gyms are open following the strict rule of ROIC >30%, the greater the operating margin. However, the more gyms are opened and immature, the more compressed free cash flow will be as it takes 30 months for those gyms to reach maturity (and thus full profitability). As of June 2025, there were 1,628 gyms open, of which only 1,175 were mature. Therefore, almost 500 gyms are still not fully profitable. Yes, there is a lot of profit hidden that will appear in the next 12 to 24 months by doing nothing, just waiting. And that will push the operating margin clearly north of 10%.

The hidden gold: mature gyms brought in on average EUR 400k of Club EBITDA, immature clubs about EUR 65k only. This leads to a Club EBITDA less rent of EUR 465m at YE24. If all the 1,575 clubs at YE24 were mature, Club EBITDA less rent would have been EUR 628m. That is more than a EUR150m of earnings growth which will happen by just doing nothing and waiting for those gyms to mature. I will show the numbers in the valuation section to see how Basic Fit’s valuation is hidden.

Licensing & Clever Fit acquisition: Basic Fit has long been discussing licensing. It is a sound option for them because the licensed gyms could operate using Basic Fit’s own software, the existing proven operating model and buy equipment by the wholesale orders placed at group level, benefitting from the group discount. For Basic Fit that means taking a fee from each licensed gym and expanding its business without capital constraints - which is currently the limitation. In 5-10 years this leads to a business that is far more capex-light and with higher profitability than today. An example is US based Planet Fitness, which largely operates a licensing model.

Linked to this, Basic Fit acquired Clever Fit in October 2025, which owns 39 clubs in Germany and Austria and has 454 franchisees across Europe - primarily the DACH region. This is an automatic fit for Basic Fit as it opens the whole central European market. Combined, Basic Fit will have more than 2,000 clubs in Europe with a blended model of owned gyms and capital light franchises. It will likely accelerate the franchise option because by buying Clever Fit, it has also brought in expertise in franchising. Clever Fit earns EUR 50m a year in revenue with EBITDA of EUR 14.5m which was bought for EURO 160m + EUR 15m possible earnouts. That is 11x EBITDA, above the 7.5 at which Basic Fit trades. However, there is a clear premium related to the strategic importance of the move and the franchising optionality it unlocks right off the bat.

Competition

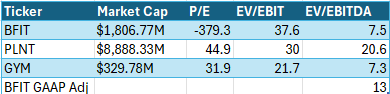

There are not many gym chains listed unfortunately, so the peer group is rather thin. On the low-cost section, there are several gym chains as shown above, however not that many at the scale of Basic Fit other than Pure Gym, and that is a UK company. However, there are many gyms out there in general, which means that customers have the choice of where to go with varying price points and services offered. Competition is meaningful. This forces Basic Fit to maintain competitive pricing to ensure it is always amongst the cheapest. There are two comparable companies in the market, The Gym Group, a smaller Gym chain in the UK that operates a low cost model, and Planet Fitness, the massive gym chain in the US. The difference with Planet Fitness is that they operate a large franchise model, which makes it harder to compare with Basic Fit.

Now, the financials are difficult to compare. As I mentioned above, Basic Fit is reinvesting heavily so EV/EBIT is not a great measure unless I normalise all 3 gyms to compare them. Then, EV/EBITDA which would be better (and can be used to compare BFIT and GYM) is useless to compare it with Planet Fitness because they report under US GAAP and Basic Fit under IFRS. Leases are treated differently and makes it incomparable. If I adjust to remove leases above EBITDA at Basic Fit, I get an EBITDA of EUR 339m. That leads to an EV/EBITDA of 13 times compared to 20.6 times Planet Fitness. Yes, on a like for like basis Basic Fit is dirty cheap compared to Planet Fitness!

Review of financial performance

Basic Fit was heavily impacted by the Covid crisis, leading to heavily distorted gym performance for couple of years, which has also impacted its balance sheet. Therefore, I will show recent years to highlight the trend.

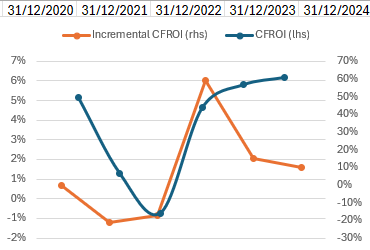

Below we have 2 measures: CFROI or Cash From Operations divided by Capital Employed (blue, lhs) and Incremental CFROI (orange, rhs), which measure the changes in CFROI and is an excellent measure of how recent capital is generating returns. Since the covid debacle, CFROI is increasing steadily. This is a lagging indicator as it incorporates past information but if it increases it means that recent CFROI is higher than previous ones. However, Incremental CFROI has jumped to double digit territory and that is what matters. Capital employed over the last 3 years is returning >10% on investment, which over time is what shareholders should expect to receive.

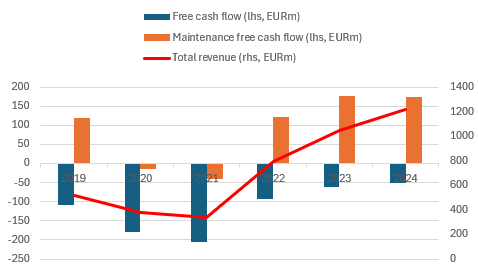

As I have mentioned, Basic Fit is reinvesting heavily into its business. Therefore, free cash flow is usually slightly negative. However, management is choosing to use its free cash flow to put it back into growth and future larger cash flow. The below graph shows maintenance cash flow, which is free cash flow less growth capital expenditures, as well as total revenues and free cash flow since 2019. Clearly, Basic Fit makes good money as shown by the orange columns. It just hides as its all reinvested leading to the blue columns. Maintenance free cash flow is an excellent perspective into how much free cash flow a business that will not grow actually makes.

In terms of share price performance, shareholders invested prior to the Covid crisis have not done very well. That is why price paid matters. However, today it is as cheap as its ever been wile the business is as good as its ever been.

Management and shareholders

The founder Rene Moos is still the CEO. He owns 11.8% of the shares, which ensures alignment with investors. Having him at the helm of the company provides comfort to outside investors, at least to me, as his wealth is aligned to the success of the company. In addition, he as navigated the business during the Covid lockdowns, where the company could have been at risk of ceasing operations. With his experience and his stake in Basic Fit, he is now enjoying growing the business like he always wanted to do it.

Competitive advantages (Porter’s 5 forces)

The overall assessment is a narrow to moderate: there are some competitive advantages for this business.

Threat of new entrants

No competitive advantage . Any individual or business can easily set-up a gym and compete with Basic Fit.

Bargaining power of suppliers

Large competitive advantage: Basic Fit being the largest gym chain in Europe allows them to buy in bulk gym equipment at competitive prices. This creates a competitive advantage against smaller gym chains that have to pay full price.

Bargaining power of buyers

No competitive advantage: gym users can choose between Basic Fit and other gyms at little cost.

Threat of substitutes

No competitive advantage . It is easy to substitute Basic Fit as a gym user by another gym chain at little cost.

Rivalry amongst competitors

Narrow competitive advantage. Basic Fit competitors will struggle to compete in price while maintaining profitability. It happens, but Basic Fit has some edge in the scale it has achieved.

Valuation

Discounted Cash Flow model

I value Basic Fit based on a DCF model first, my favoured approach. The assumptions are that by end-2028 it reaches 1,978 gyms with per Club EBITDA at EUR 370k, of which mature clubs at EUR 430k. I discount cash flows at 10%, my hurdle rate, and apply a terminal growth of 2%. Therefore, in 2028 Basic Fit would make EUR 1.9bn in revenues, EUR 510m in cash from operations, and a maintenance free cash flow (with no growth capex) of EUR 363m - which I use to derive the terminal value. Based on my estimates, I derive a share price closer to EUR 40, far above the current share price of EUR 23.

Earnings growth

Another way is is to calculate the EBIT growth rate with the Return On Capital Employed (ROCE) multiplied by the Reinvestment Rate (RR). This should yield the approximate EBIT growth for a company. In the case of Basic Fit while volatile due to the Covid impact, the RR has been above 100% with acquisitions at a recent ROCE of 10%-15%, which should untap plenty of earnings growth. This is in line with my expectations of immature gyms unlocking free cash flow over the next 2 years whilst Basic Fit hides its cash flow in the form of capex to open new gyms (or franchises).

EBITDA exit multiple

Finally, based on an EBITDA exit multiple in 2028, setting it at 9x EBITDA (less rent) the return that I would expect is of 15% / year, above my 10% hurdle rate. Today Basic Fit trades at 7.5x EBITDA, so this implies a re-rating albeit relatively modest. Without re-rating, the return would be 9.2% / year. But by that point they can just buy back stock at an incredible yield.

FCF yield

Another perspective is to take into account the yield on this investment from the cash flow it generates. The Enterprise Value is around EUR 2.8bn today, and free cash flow ex growth capex (maintenance free cash flow) in 2026 should be around EUR 280m. That is a 10% yield.

Catalysts and risk factors

Catalysts

There are nature tailwinds to gyms driven by health benefits and a general gym membership under penetration in Europe. Moreover, Basic Fit’s scale allows it to reinvest meaningfully in new gyms faster than competitors while taking market share. The franchise option unlocks a capital-light option to earning future revenues in a capital-light manner.

Risk factors

Planet Fitness could put up fierce competition in some markets. In addition, a cost-of-living crisis that deepens could put at risk memberships and limit pricing power at Basic Fit. Finally, execution risk such as failure to reach profitability in certain markets or to integrate successfully new acquisitions could hurt the business in the long-term.

Investment thesis

Basic Fit has scale and makes substantial money of its gyms. However, its constant reinvestment into the business hides the free cash flow it generates. If the market notices Basic Fit again as the well managed growing business it is and that it has largely overcome the impact of Covid, the market multiple could change substantially. Regardless, Basic Fit keeps growing, keeps becoming more profitable and keeps gaining scale. It has the ingredients for a long-term compounder: reinvesting all its earnings at a higher-than-average return on investment. Regardless of what the market does, this is a strong candidate for a sit-and-wait and let it compound over years.

Disclaimer

This post is written by Miguel Maeztu, known as AzeriaInvest on eToro. Cristia Calle, known as CCalle is part of CM Capital Research. You can find us here:

Cristia Calle Mercado - eToro Popular Investor | https://etoro.tw/4lPaH5z

Miguel Maeztu - eToro Popular Investor | https://etoro.tw/3JGPmxS

Copy Trading is not investment advice | Capital at risk | Past performance does not guarantee future results.

Informational only: This analysis is for information/education and is not investment, legal, accounting, or tax advice, nor a recommendation to buy or sell any security. CM Capital Research is not acting as an advisor or fiduciary.

Risks: Investing involves risk, including loss of principal. Past performance does not guarantee future results. Any forward‑looking statements are uncertain and may change without notice.

Accuracy: Information may be incomplete or inaccurate. No warranty is made regarding timeliness or completeness.

Conflicts: The Author(s) and affiliates may hold, buy, or sell the securities mentioned without notice.

No offer: This is not an offer or solicitation in any jurisdiction where it would be unlawful. Consult a qualified professional for personalized advice.

Miguel, is there anything Basic Fit does differently in its approach to the customer in the gym, anything that can differentiate them from other low cost operators? Something in the human to human approach, something that can increase customer retention and loyalty?