Adyen N.V. (ADYEN.AS)

A review of Adyen

Executive summary

Adyen is a leading European payments services provider

Adyen faces secular industry growth while taking wallet share form rivals

Quality company with a 45% - 50% operating margin

Stock price is down 40% in the past year

Strong balance sheet with healthy net cash position

Introduction

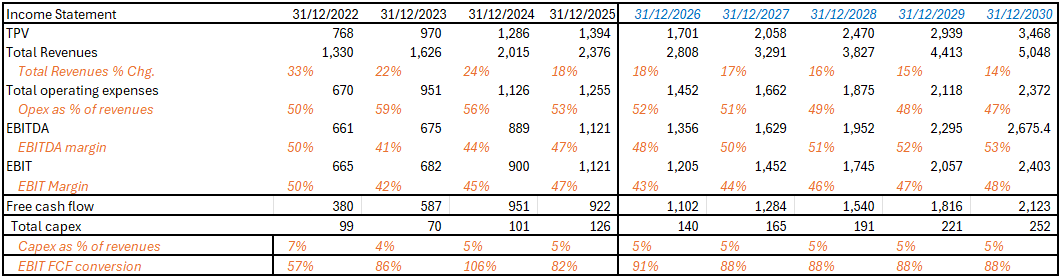

Adyen is an end-to-end payment processing company offering its services to online, in-store and mobile transactions. Founded in 2006 in Amsterdam by Pieter van der Does and Arnout Schuijff, Adyen emerged from the founders' prior success with Bibit, an online payments firm they sold. The name "Adyen," from Sranan Tongo meaning "start again". In 2009, Adyen signed its first major client, Groupon, marking enterprise traction. By 2012, it expanded globally with offices in San Francisco, Paris, and London, while securing a pan-European acquiring license and adding POS services. Adyen went public on Euronext Amsterdam in 2018, under ticker ADYEN, priced at €240 per share in a €849 million offering that valued it at €7.1 billion. In 2025, it processed a Total Payments Volume (TPV) of EUR 1.39tn, had an EBITDA margin of almost 53% and an operating margin of over 47%.

3-liner summary rule

Adyen is an end-to-end payments provider that benefits from secular industry growth while taking market share from legacy payment companies thanks to its superior product. High margin, superior offering, double digit ROIC and pristine balance sheet are supportive of long-term shareholder returns.

Business model

Operating markets

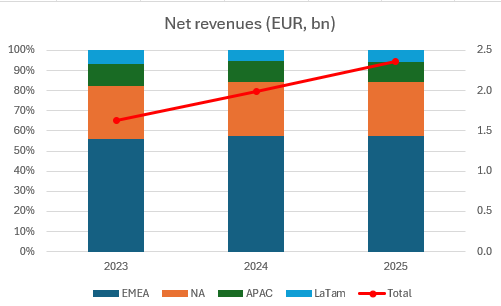

Geographically Adyen operates worldwide, however EMEA and the North America make up the bulk of their revenues. While it has taken a strong foothold in Europe, it is pushing to grow in North America, where it faces other newer entrants as well as large legacy providers.

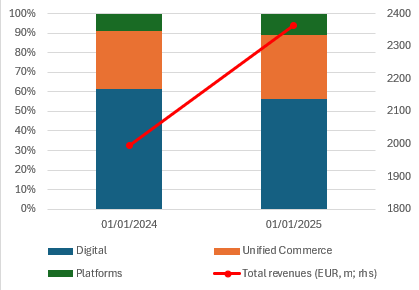

By type of client offering, Adyen breaks down its segments as Digital, Unified Commerce and Platforms.

Under Digital, Adyen focuses on online and mobile payments for e-commerce platforms and DTC companies like Netflix. Under Unified Commerce, Adyen combines online and physical (POS) payments for omnichannel retailers, the likes of Starbucks or H&M. Finally, under Platforms Adyen offers additional services such as data insight, risk management, treasury tools that leverage Adyen’s ecosystem. Some of Adyen’s clients include well-known names such as Uber, Netflix, eBay, Spotify, Lidl and Starbucks.

Market positioning

Adyen’s product is positioned in the whole payment processing stack and is competitively priced. Adyen has favoured the medium to larger client with a price (take rate) that declines over time and with scale in order to strengthen the stickiness of its products and limit customer churn. It excels with enterprise-scale and omnichannel integration for high-volume merchants. Therefore, it acts (can act) as acquirer, gateway and processor, supporting an multitude of payment methods from cards (Visa, Mastercard) to wallets (Apple, Google Pay) and local options.

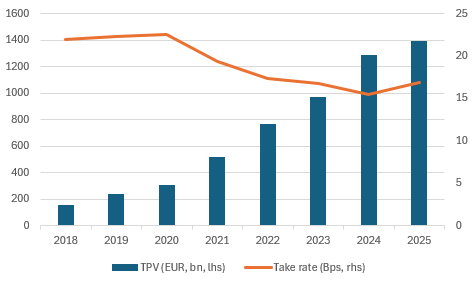

Traditionally what Adyen does with one product has been done by several companies, hence the offering increases efficiency by reducing the cost to the merchants and the speed of it. When compared to competitors, competition is strong but the superiority of Adyen against most of them is clear. In 2015 it processed EUR 23bn of TPV or 0.2% of it. In 2025 it processed 3.8% of the EUR 34tn TPV. The market is still very much fragmented, and I refer you to the previous article written by Cristia Calle on this very Substack for an overview of the payments industry.

Business economics

Adyen has one business, which is to process payments. To do that, it charges an Interchange++ pricing model with a fixed processing fee per transaction of lets say EUR 0.1 to EUR 0.15 plus a mark-up of 0.25%-0.6%. The mark-up is negotiable with scale and is a tool to strengthen customer retention over the long-term. The other costs to the consumer or merchant can come from the Issuers which issue payment cards to consumer and manage credit lines and accounts (Amex, Chase, Santander…) and the Networks which route transactions globally (Visa, Mastercard, also Amex, Discover, Apple Pay and Google Pay) in the form of an interchange fee from the card or network provider in the range of 0.3%

Ultimately, the operating Net Revenue achieved by Adyen divided by the TPV leads to the key metric: the take rate. Their fee basically. Due to the feature of progressively reducing the mark-up as the volume scales up with merchants, the take rate of Adyen over time will decrease while the TPV increases. The uptick of the take rate in 2025 is an anomaly related to the loss of a large account (Block) that was high in volume but low in take rate. This led to a slowdown in the TPV but an improvement in the take rate.

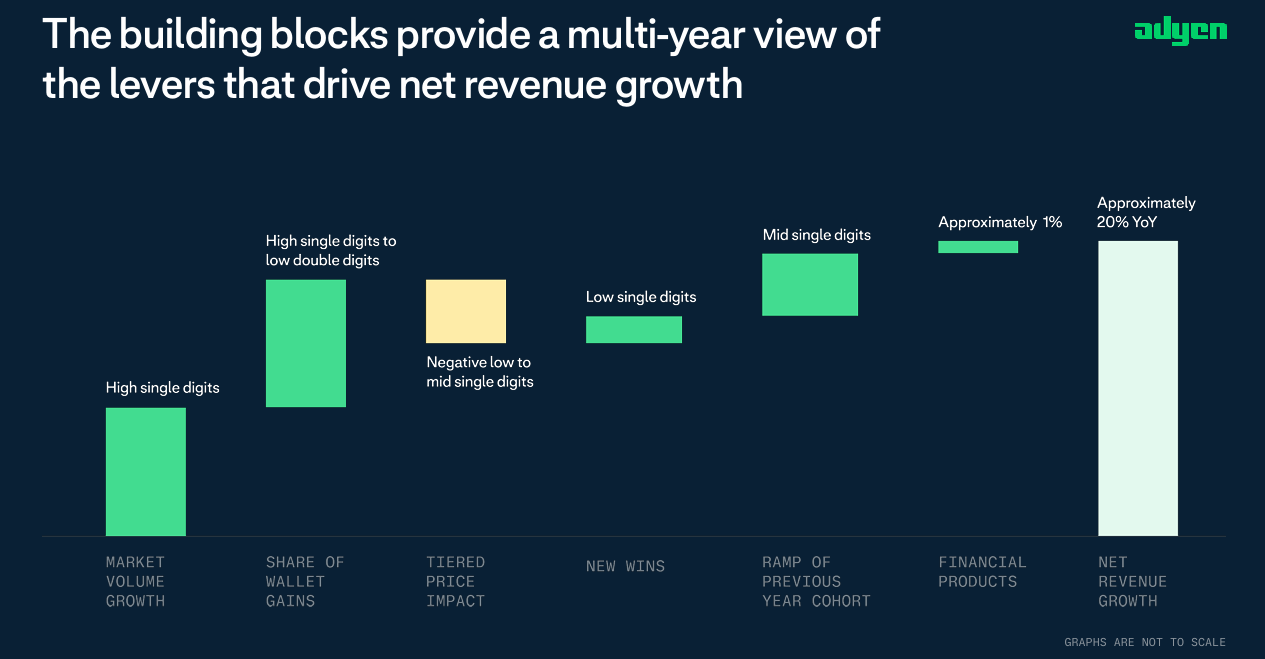

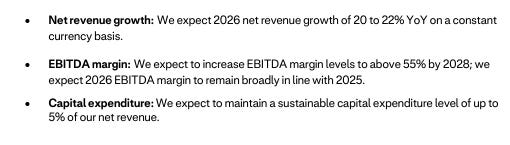

Going forward, the revenue growth levers for Adyen come from the high single digit secular growth of the payments industry, on top of which a similar figure comes from taking market share from existing competitors operating under more legacy systems, followed by the aforementioned lower progressive mark-up with clients which is a negative contributor, and then positive contributions from new clients and from higher monetisation of previous cohorts. In the end a shy 1% highlighted by Adyen from financial products comes from additional value-added initiatives linked to their banking licenses that could further monetise clients.

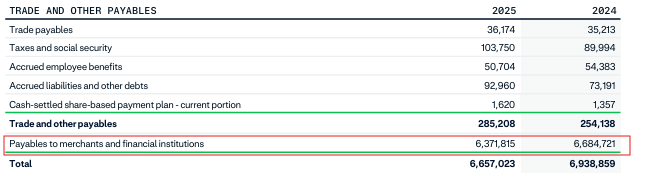

There is an important element to disclose. During the payment process, Adyen comes to hold meaningful balances of customer, or so called “In-transit” cash. This is not Adyen’s and shows as Cash and equivalents on their balance sheet, but also as a Payable to merchants and financial institutions in their balance sheet. On that, they earn a little of interest but due to the large amount of money moved, it was in the region of EUR 150-170m in 2025. Lower if interest rates go down, higher if they go up.

Competition

The environment is competitive. Because Adyen works primarily with larg(er) businesses, it competes with global payments processors for such segments.

Direct competitors are Stripe, Braintree (PayPal) or Checkout.com, that operate more modern tech stacks and are gaining new business, as well as taking business from the legacy providers. The legacy providers are also competitors, but those loose business to the likes of Adyen. WorldPay, Global Payments, Fiserv, Worldline, Nexi. Then there are wallet-centric competitors, such as PayPal Holdings (which leverages their PayPal / Venmo wallets), Block Square, the likes of Amazon Pay or Apple Pay. Cross-border payout / FX focused businesses such as Wise, Airwallex or Pioneer but this is more niche. And we can even include card schemes (Amex, Visa) and traditional banks that indirectly compete with some overlap in some of the functions, although not directly or fully competing. Therefore, clearly the first two categories are the competitive ones, with the newer players competing for new business and the legacy players giving up business for those new ones.

Review of financial performance

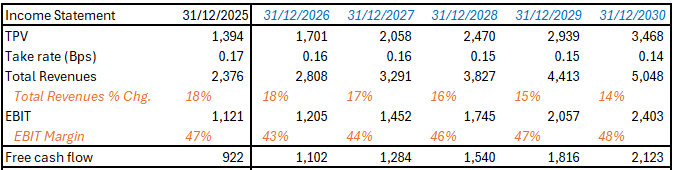

Adyen operates a relatively capital light model and a very profitable enterprise. EBITDA is in the 50% range, expected to tick upwards towards 55% in the next few years, while operating margin runs in the high 40s%, the difference being primarily depreciation, right-of-use depreciation and to some extent amortisation. Free cash flow conversion is in the 90% range.

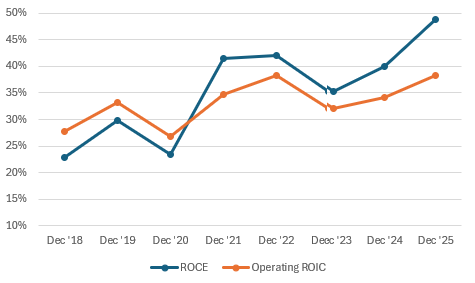

Adyen shows improving returns on capital, as measured by ROCE and ROIC. While there is some divergence in the figures due to data inputted, the trends are clear and underscore the profitability of this business. An improving ROI metric often leads to improving margins.

Since this is a business that thrives at scale and there appears to be clear above-industry growth for Adyen, I would expect management’s guidance of 55% EBITDA margin in the short term to materialise, albeit in my model I apply a cut to it and delay the improvement. Management guidance is usually the best case scenario, hence a cut to it should provide a more normalised situation.

Management and shareholders

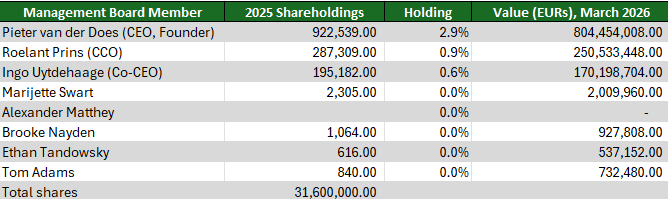

Management has skin in the game. CEO and Co-Founder Pieter van der Does has nearly EUR 1bn tied to Adyen, while the Chief Commercial Officer and the Co-CEO also hold a meaningful amount.

In addition to being insiders, Pieter has been with the company since its founding, Ingo since 2011 and Roelant since 2007 like Pieter.

In a very non-US way, the Co-CEOs and CCO receive only cash remuneration. While other members of the management board get share-based compensation in the range of 100% of the salaries (CFO, CHRO and CRCO). In effect, the 3 key insiders and managers are paid less than other key executives. Overall, the insiders show skin in the game and therefore alignment with the broader shareholder base, which greatly solves the agency problem.

Beyond the insiders, BlackRock owns almost 10% of Adyen, followed by Temasek, the Singaporean wealth fund and Ballie Gifford at 5%, the British active growth investor. Therefore, institutional shareholding is also fairly solid. Overall, management and shareholders and in my opinion a positive factor to Adyen’s investment prospects.

Competitive advantages (Porter’s 5 forces)

The overall assessment is that there are competitive advantages associated with integration, scale and network effects. However, the moat is rather narrow as there are substitutes, buyers and suppliers hold certain power over Adyen and there is competition amongst incumbents.

Threat of new entrants: low-to-moderate

Medium advantage. There are regulatory barriers in place and important up-front capex to limit new entrants. In addition, there is a network effect in that a merchant will prefer a provider already integrated with payment methods that a new one still in the make. Adyen has scale and global reach the make of this a competitive advantage.

Bargaining power of suppliers: moderate

Low to moderate competitive advantages. Card networks and issuing banks set interchange fees. It would be very difficult for Adyen to say no to Visa. Certain suppliers clearly have the upper hand since the merchant is interested in a payment processor that can process most commonly used payment methods to maximise sales. However, beyond the key very large ones, such power fades away in favour of Adyen. Adyen mitigates this with scale, as the larger it gets, the bigger a customer of issuers and card networks it becomes. In addition, enabling payment methods de-risks dependence from one single issuer or network such as Amex or Visa.

Bargaining power of buyers: moderate-high

No competitive advantage: Merchants have alternatives, therefore can push-back against fee hikes or can threaten with changing provider. While cross-selling and switching-costs cap to a certain extent the power of merchants, the balance of power sits with the merchants. For Adyen, progressive pricing is a meaningful mitigant here.

Threat of substitutes: moderate

Low competitive advantage. Substitutes are available, from other payment processors to cash to closed-loop wallets. The actual substitute might note fully replace Adyen, but there is nothing unique and exclusive or proprietary to Adyen to create an advantage here.

Rivalry amongst competitors: high

No competitive advantage. There is heavy competition amongst incumbents, with somewhat limited pricing power beyond a certain range. Rivals are well-position and capitalised (Stripe, Braintree, Fiserv…)

Valuation

DCF

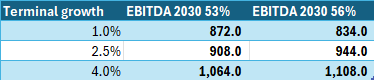

I apply a simple valuation method by following a Discounted Cash Flow (DCF) model valuation. I apply the margins and indicators stated above in the Financial Performance section and in the summary table above. I use my hurdle rate and benchmark as discount rate: 10%. And I apply a terminal growth of 2.5% - on the generous end but industry growth justifies it in this case. The DCF leads to an Enterprise Value of EUR 23.4bn, which accounting for a Net Cash of EUR 4.4bn results in a per share intrinsic value of EUR 908, very close to today’s share price of EUR 870. By playing with the EBITDA margin in 2030 and the terminal growth rate the result is as follows.

As of today the stock could provide that sough-after 10% annualised return over time. however, the margin of safety is not huge.

Catalysts and risk factors

Catalysts

Growth and scale keep increasing switching costs and improving efficiency metrics

Cross-selling options can further widen the moat

Wallet gains from legacy rivals and new customers to keep fuelling growth

Risk factors

Increased price competition could add further pressures to the take rate

Lower industry growth and rival customer stickiness could thwart 20%/year target growth and impact valuations

Unexpected insider sells could lower skin in the game

Investment thesis

Adyen operates an end-to-end payment processing stack with a superior offering to legacy payment providers. It operates at scale and worldwide, catering to the higher end of corporates. 20% revenue growth is fuelled by a combination of single digit industry growth and by taking walled share from existing legacy providers - a trend that should be valid for the foreseeable future. The take-rate will decrease over time as Adyen operates a progressive pricing policy with higher payment volume, which also increases customer retention. Key insiders hold meaningful stakes in the business, solving the agency problem and creating alignment with its shareholder base. By achieving 20% revenue growth yearly and achieving a 55% EBITDA margin in the short term, Adyen should be able to deliver at least a 10% annualised rate of return to shareholders.

Disclaimer

This post is written by Miguel Maeztu, known as AzeriaInvest on eToro. Cristia Calle, known as CCalle is part of CM Capital Research. You can find us here:

Cristia Calle Mercado - eToro Popular Investor | https://etoro.tw/4lPaH5z

Miguel Maeztu - eToro Popular Investor | https://etoro.tw/3JGPmxS

Copy Trading is not investment advice | Capital at risk | Past performance does not guarantee future results.

Informational only: This analysis is for information/education and is not investment, legal, accounting, or tax advice, nor a recommendation to buy or sell any security. CM Capital Research is not acting as an advisor or fiduciary.

Risks: Investing involves risk, including loss of principal. Past performance does not guarantee future results. Any forward‑looking statements are uncertain and may change without notice.

Accuracy: Information may be incomplete or inaccurate. No warranty is made regarding timeliness or completeness.

Conflicts: The Author(s) and affiliates may hold, buy, or sell the securities mentioned without notice.

No offer: This is not an offer or solicitation in any jurisdiction where it would be unlawful. Consult a qualified professional for personalized advice.

Thanks for reading! Subscribe for free to receive new posts and support our work.

Company we’re actively researching in the payments sector!